TL;DR:

- Affordable transfer pricing involves setting intercompany transaction prices that meet the arm’s-length standard while minimizing compliance costs for documentation and analysis. It emphasizes selecting reliable methods, maintaining contemporaneous documentation, and ensuring consistent agreements to reduce audit risks and expenses. Proper planning and strategic approach help businesses avoid costly pitfalls and build a cost-effective transfer pricing framework.

Affordable transfer pricing is defined as the practice of setting intercompany transaction prices that satisfy the arm’s-length standard while keeping total documentation and compliance costs financially manageable. Every business with related-party transactions, whether a multinational corporation or a growing small business with a foreign subsidiary, must price those transactions as if they were between independent parties. The OECD guidelines and IRS regulations both require this. The real challenge is not understanding the rule. The challenge is meeting it without spending more on compliance than the tax savings justify.

What is affordable transfer pricing and why does it matter?

Transfer pricing sets prices for transactions between related entities within the same corporate group, directly affecting how profits are allocated across jurisdictions and what taxes each entity owes. When a U.S. parent company charges its Canadian subsidiary for management services, that charge is a transfer price. Tax authorities in both countries scrutinize it. The goal of affordable transfer pricing is not to cut corners on compliance. The goal is to meet the legal standard at a cost proportional to the tax risk involved.

The industry term for this discipline is simply “transfer pricing,” but the affordability dimension is what separates reactive, expensive compliance from proactive, cost-efficient strategy. Businesses that treat transfer pricing as an afterthought often face audit adjustments, penalties, and the cost of rebuilding documentation under pressure. Businesses that plan ahead select the right methods, maintain lean documentation, and use OECD-approved simplifications where available.

Three factors determine whether your transfer pricing approach is truly affordable. First, method selection must produce a defensible arm’s-length result without requiring comparables data that costs more to obtain than the risk warrants. Second, documentation must be sufficient to withstand an audit without being exhaustive. Third, the pricing policy must be consistent with actual business operations, because inconsistency is the most common trigger for costly disputes.

What is the arm’s-length principle and why is it central?

The arm’s-length principle requires that conditions in related-party transactions match what independent parties would agree to under comparable circumstances. This standard is codified in OECD Model Tax Convention Article 9 and forms the legal backbone of transfer pricing rules in over 140 countries.

Understanding this principle matters for affordability because it defines the target. You are not trying to find the lowest possible price or the highest defensible markup. You are trying to find the price a real market transaction would produce. The closer your intercompany price is to that market reality, the less documentation you need to justify it.

Key requirements under the arm’s-length principle include:

- Comparability: The related-party transaction must be compared to genuinely similar uncontrolled transactions, accounting for differences in functions, assets, risks, and contractual terms.

- Reliability: The chosen comparable must reflect economic reality, not just surface similarity. A gross margin comparison between a full-risk distributor and a limited-risk distributor is not reliable.

- Consistency: The same method and pricing policy should apply year over year unless business circumstances change materially.

- Documentation: The analysis supporting the arm’s-length conclusion must be contemporaneous, meaning prepared before or at the time of filing, not reconstructed after an audit notice arrives.

The affordability insight here is that a well-chosen comparable reduces documentation burden. When your intercompany price closely mirrors a publicly available market price, the analysis is short and defensible. When the comparable is weak, you compensate with volume, and volume costs money.

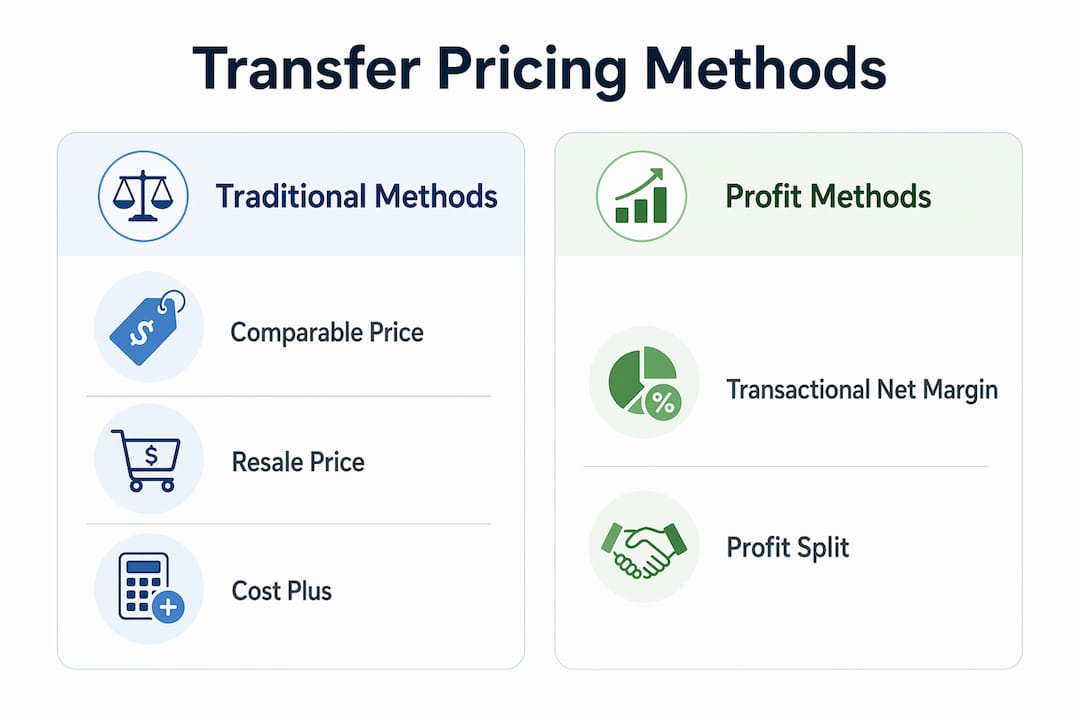

What transfer pricing methods are considered affordable and defensible?

OECD-approved methods fall into two categories: traditional transaction methods and transactional profit methods. Each carries a different cost profile and a different evidentiary standard.

The five primary methods are compared below:

| Method | Best use case | Data requirement | Relative cost |

|---|---|---|---|

| Comparable Uncontrolled Price (CUP) | Commodity transactions, loans, royalties | High: requires near-identical comparables | Low if data exists |

| Resale Price Method | Distribution with limited value-add | Moderate: gross margin comparables | Moderate |

| Cost Plus Method | Manufacturing, contract services | Moderate: cost base plus markup | Moderate |

| Transactional Net Margin Method (TNMM) | Most service and distribution transactions | Lower: net margin databases widely available | Moderate to high |

| Profit Split Method | Highly integrated transactions, unique intangibles | Very high: requires detailed profit attribution | High |

The Comparable Uncontrolled Price method takes precedence when reliable data exists. A loan between related parties priced at a published benchmark rate, for example, is cheap to document and nearly impossible to challenge. The TNMM is the most frequently used method in practice because net margin data from commercial databases like Bureau van Dijk or Dun and Bradstreet is widely available. However, TNMM is not automatically correct just because data is accessible. Using it when a traditional method would produce a more reliable result is a common and expensive mistake.

Pro Tip: Before committing to TNMM for a service transaction, ask whether a cost-plus analysis using your own cost data would produce a more reliable result. Your internal data is free. External database subscriptions are not.

Method selection drives total compliance cost more than any other single decision. A method that looks cheap upfront because the data is easy to find can produce an unreliable result that requires expensive rework during an audit.

How can businesses reduce transfer pricing documentation costs?

Reducing documentation costs without sacrificing defensibility requires a structured approach. The OECD has provided one significant tool for service transactions: the simplified approach for low-value-adding intra-group services, commonly called the LVAS approach.

Under the LVAS approach, qualifying support services such as accounting, human resources, and IT support can be priced using a fixed 5% markup on costs without a full benchmarking study. This eliminates the need for external comparables searches for those service categories. The catch is that this approach is elective and jurisdiction-dependent. If the country where your subsidiary operates has not adopted the OECD model locally, you cannot use it there and must conduct full analysis instead.

A practical documentation workflow for affordable transfer pricing compliance follows these steps:

- Conduct a functional analysis first. Identify which entity performs which functions, holds which assets, and bears which risks. Tax auditors focus on this analysis above all else. A clear, accurate functional analysis reduces the volume of supporting evidence you need everywhere else.

- Select the method based on reliability, not convenience. Document your reasoning for rejecting alternative methods. This rejection analysis is required under most OECD-aligned regimes and protects you if an auditor prefers a different method.

- Prepare contemporaneous documentation. In the U.S., documentation must be produced within 30 days of an IRS request to protect against penalties reaching up to 40% of the underpayment. Waiting until after an audit notice is issued eliminates penalty protection entirely.

- Apply the benefit test for all service charges. Every intercompany service charge must demonstrate that the recipient received a genuine economic benefit. Failing this test forces full benchmarking and eliminates the cost savings from simplified approaches.

- Maintain intercompany agreements aligned to your documentation. A legal agreement that contradicts your functional analysis is a red flag in any audit. Keep agreements, documentation, and actual conduct consistent.

Pro Tip: Treat your transfer pricing documentation as a living file, not an annual project. Updating it quarterly takes two hours. Rebuilding it under audit takes two months and costs significantly more.

Penalty risks and under-documentation significantly raise total compliance costs, so investing reasonably in documentation upfront almost always reduces net expenses over a three-year audit cycle.

What are common pitfalls in affordable transfer pricing?

The most expensive transfer pricing mistakes are not the ones that look risky. They are the ones that look efficient.

- Choosing a method for data availability rather than reliability. Comparability defects in the chosen comparable can require complete rework during an audit, turning a low-cost analysis into a high-cost dispute.

- Skipping the functional analysis. A thin or generic functional analysis is the single most common reason tax authorities reject transfer pricing documentation. Without it, every other element of the documentation is weakened.

- Failing the benefit test on service charges. If your subsidiary pays a management fee but cannot demonstrate what it received in return, the charge fails the benefit test. This forces full benchmarking and eliminates affordability advantages from simplified approaches.

- Applying OECD simplifications in non-adopting jurisdictions. Using the LVAS fixed markup in a country that has not adopted the model creates a compliance gap that auditors will find.

- Inconsistent intercompany agreements. When the legal agreement says one thing and the actual transaction does another, auditors recharacterize the transaction. Recharacterization is expensive to defend and often results in double taxation.

Each of these pitfalls increases total compliance cost, often by more than the original documentation savings. The pattern is consistent: short-term cost cuts in transfer pricing create long-term audit exposure.

How to apply affordable transfer pricing principles in practice

A practical, affordable transfer pricing framework centers on clear functional analysis, method rationale, and a comparables trail that auditors can follow without extensive explanation. Businesses that build this framework into their annual financial planning cycle spend less on compliance and face fewer disputes.

Practical steps to integrate transfer pricing into your financial strategy:

- Design intercompany agreements before transactions occur, not after year-end. Retroactive pricing adjustments are a major audit trigger.

- Assign transfer pricing ownership to a specific person in finance, not to external advisors alone. Advisors are expensive. Internal ownership keeps costs down.

- Review your pricing policy annually against actual margins. If your subsidiary’s actual results fall outside your documented arm’s-length range, make a year-end adjustment before filing.

- Leverage OECD simplified approaches for qualifying service transactions in jurisdictions that have adopted them, and document the jurisdictional adoption as part of your file.

- Coordinate transfer pricing with your overall tax planning. A pricing policy that reduces transfer pricing risk but creates a permanent establishment in a high-tax jurisdiction is not affordable in total.

The businesses that manage transfer pricing most cost-effectively treat it as a financial planning discipline, not a tax compliance checkbox.

Key takeaways

Affordable transfer pricing requires reliable method selection, contemporaneous documentation, and consistent intercompany agreements to contain compliance costs and penalty risk.

| Point | Details |

|---|---|

| Arm’s-length principle is non-negotiable | All intercompany prices must reflect what independent parties would agree to under comparable conditions. |

| Method selection drives total cost | Choosing a method for data convenience rather than reliability creates expensive audit exposure downstream. |

| LVAS simplification reduces service costs | The OECD fixed 5% markup for low-value services eliminates benchmarking costs where jurisdictions have adopted it. |

| Contemporaneous documentation prevents penalties | U.S. rules require documentation available within 30 days of IRS request to avoid penalties up to 40%. |

| Benefit test is mandatory for service charges | Every intercompany service fee must demonstrate genuine economic benefit to the recipient or full benchmarking is required. |

Why I think most businesses get transfer pricing backwards

Most finance teams I have seen treat transfer pricing as a compliance cost to minimize. They hire the cheapest advisor, produce the thinnest documentation that seems defensible, and move on. That approach is rational in year one. It becomes irrational the moment an auditor opens the file.

The businesses that spend the least on transfer pricing over a five-year period are not the ones who spent the least in year one. They are the ones who built a clean, consistent framework early and maintained it with minimal annual effort. The upfront investment in a solid functional analysis and a well-reasoned method selection pays for itself the first time an audit inquiry arrives and you can respond in days rather than months.

The other mistake I see consistently is treating OECD simplifications as a universal shortcut. The LVAS approach is genuinely useful, but only where it applies. Applying it in a jurisdiction that has not adopted the model is not a cost-saving strategy. It is a compliance gap waiting to be found. Knowing which simplifications your specific jurisdictions have adopted is not optional. It is the foundation of any budget-friendly transfer pricing strategy that actually holds up.

My honest recommendation: spend the money once on a proper functional analysis and method selection. Then maintain it yourself with quarterly updates. That is the most affordable transfer pricing approach available to any business, regardless of size.

— Anthony

Affordable printing solutions from Transferkingz

At Transferkingz, we understand that balancing quality and cost is a real business decision, not just a tax concept. Whether you are managing intercompany pricing strategy or looking for cost-effective custom printing for your business, the principle is the same: get the best defensible result at a price that makes sense for your operation. Transferkingz offers DTF transfer services in Texas with no minimum order requirements, fast turnaround, and premium quality that small businesses and production shops rely on. Explore our services and see how affordable quality actually looks in practice.

FAQ

What is affordable transfer pricing in simple terms?

Affordable transfer pricing means setting prices for transactions between related business entities at arm’s-length rates while keeping the cost of documentation and compliance proportional to the tax risk involved. The goal is legal compliance without excessive expense.

What is the arm’s-length principle in transfer pricing?

The arm’s-length principle requires that related-party transaction prices match what independent parties would agree to under comparable conditions. It is the legal standard under OECD Model Tax Convention Article 9 and applies in over 140 countries.

Which transfer pricing method is the most cost-effective?

The Comparable Uncontrolled Price method is the most cost-effective when reliable comparable data exists, because it requires minimal documentation. The TNMM is widely used due to data availability, but it is not automatically the cheapest option when comparability defects require extensive adjustments.

How does the OECD LVAS simplification reduce transfer pricing costs?

The OECD simplified approach for low-value-adding intra-group services allows a fixed 5% markup on qualifying support services without a full benchmarking study. This applies only in jurisdictions that have adopted the model locally, so confirming local adoption is required before using it.

What penalties apply for inadequate transfer pricing documentation in the U.S.?

The IRS can impose penalties up to 40% of the tax underpayment for transfer pricing adjustments. Contemporaneous documentation that meets IRS requirements and is produced within 30 days of request provides the primary defense against these penalties.

Recommended

- Maximize custom apparel success with transfer application guides – Transfer Kingz

- Affordable Bulk DTF Transfers for Your Business Needs: Quality, Speed, – Transfer Kingz

- Affordable Bulk DTF Transfers for Your Business Needs: Quality, Speed, – Transfer Kingz

- Are Bulk DTF Transfers Worth It? Cost, Benefits, and Comparison for Bu – Transfer Kingz

0 comments